Retirement Plans for Rockwall Business Owners

Overview of Solo 401(k), SEP, SIMPLE, Traditional & Roth IRAs, defined benefit and profit‑sharing plans for Rockwall business owners — limits, tax treatment, and admin.

Retirement Plans for Rockwall Business Owners

Running a business in Rockwall comes with challenges, and planning for retirement often takes a backseat. Yet, having a retirement plan is crucial - not just for securing your future but also for attracting top talent. Here’s a quick look at options tailored to business owners like you:

- Solo 401(k): Ideal for self-employed individuals or those with only a spouse as an employee. High contribution limits ($72,000 in 2026) and tax advantages.

- SEP IRA: Simple to set up, with contributions up to 25% of compensation or $70,000. Best for businesses of any size without complex employee benefits.

- SIMPLE IRA: Designed for small businesses with 100 or fewer employees. Lower contribution limits but easy to manage.

- Traditional IRA: Straightforward option for individuals, with a $7,500 contribution limit in 2026.

- Roth IRA: Offers tax-free withdrawals in retirement. Income limits apply.

- Defined Benefit Plan: Provides a fixed retirement income, allowing for large contributions but requiring higher administrative costs.

- Profit-Sharing Plan: Flexible contributions tied to business profits, with a $70,000 cap per employee.

Each plan has its own eligibility rules, tax benefits, and administrative requirements. Choosing the right one depends on your business size, employee count, and financial goals.

Retirement Plan Comparison for Rockwall Business Owners: Contribution Limits and Key Features

Best Small Business Retirement Plans: Solo 401(k), SEP IRA, Simple IRA, and 401(k) Explained

sbb-itb-bbaa742

1. Solo 401(k) Plans

If you're a Rockwall business owner working solo or with just your spouse, a Solo 401(k) could be an excellent option for retirement savings. This plan is specifically designed for business owners without common-law employees.

Contribution Limits (2026 IRS Limits)

Solo 401(k) plans offer some of the highest contribution allowances available. In 2026, you can defer up to $24,500 as an employee, which is an increase from $23,500 in 2025. On top of that, you can contribute as the employer, bringing your total contribution limit to an impressive $72,000 for the year. If you're 50 or older, you can add an additional $8,000 in catch-up contributions. And for those aged 60 to 63, there's a "super catch-up" contribution of $11,250 available.

"Higher [401(k)] deferral limits are helpful, but only if contributions are actually adjusted." - Joon Um, Certified Financial Planner, Secure Tax and Accounting

Check the eligibility criteria below to confirm your business qualifies.

Eligibility Requirements

Solo 401(k) plans are flexible and can accommodate businesses structured as sole proprietorships, partnerships, or corporations. The main condition? You can't have any employees other than yourself and your spouse. If you hire even one part-time employee who meets plan eligibility rules, the plan loses its one-participant status. Another important detail: the plan must be adopted by the tax filing deadline, even if it's established after the tax year ends.

Administrative Costs

One of the perks of a Solo 401(k) is its simplicity. There's no need for annual nondiscrimination testing since there are no additional employees to factor in. Many providers offer these plans with minimal or even no setup and maintenance fees. However, if your plan assets hit $250,000 or more by year-end, you'll need to file IRS Form 5500-EZ.

Tax Advantages

Solo 401(k) plans come with notable tax benefits. You can choose to make pre-tax contributions, which lower your taxable income, or opt for Roth contributions for tax-free growth down the line. There's also no requirement to contribute annually, giving you the flexibility to save more during profitable years and pull back when business slows. Acting as both employee and employer, you can maximize deductions and grow your retirement fund significantly - far beyond the $7,500 limit of standard IRAs for 2026.

2. SEP IRA Plans

A SEP IRA gives Rockwall business owners a straightforward and flexible way to save for retirement without the hassle of excessive paperwork. Many Rockwall area businesses find this simplicity ideal for their growth stages. Employers - whether they’re running a corporation, partnership, or working as sole proprietors - can set one up using IRS Form 5305-SEP, and there’s no need for annual Form 5500 filings. Let’s break down the key features of a SEP IRA.

Contribution Limits (2026 IRS Limits)

For 2026, the maximum contribution limit is expected to follow 2025 guidelines: the lesser of 25% of compensation or $70,000. Contributions are calculated based on a compensation cap of $350,000. Unlike Solo 401(k) plans, SEP IRAs don’t allow employee salary deferrals or catch-up contributions. Instead, all contributions come directly from the employer.

Eligibility Requirements

Employees eligible for a SEP IRA must meet these criteria: they must be at least 21 years old, have worked for the employer during 3 of the last 5 years, and earned a minimum of $750 (2024–2025 threshold). Employers can choose to ease these restrictions, such as lowering the age requirement to 18 or allowing immediate participation. However, if you contribute to the plan, you must contribute the same percentage of compensation for all eligible employees. Contributions are fully vested immediately.

Administrative Costs

One of the biggest perks of a SEP IRA is its simplicity and low cost. Setting it up is inexpensive, especially if you use the IRS model form or a prototype plan. Additionally, there’s no annual filing requirement, unlike 401(k) plans, which helps keep ongoing administrative expenses to a minimum.

Tax Advantages

Contributions made to a SEP IRA are entirely tax-deductible on your business tax return, and the earnings grow tax-deferred until withdrawn. Another benefit? Employers aren’t obligated to contribute every year, providing flexibility during tighter financial periods. Keep in mind, though, that withdrawals made before age 59½ are subject to income tax and may also face a 10% penalty.

3. SIMPLE IRA Plans

A SIMPLE IRA (Savings Incentive Match Plan for Employees) is a solid option for businesses with 100 or fewer employees who earned more than $5,000 in the previous year. The IRS recommends it for start-up employers who don’t already have a retirement plan in place. For Rockwall business owners looking for a straightforward alternative to a 401(k), the SIMPLE IRA could be a fitting choice. Here are the key details about how this plan works.

Contribution Limits (2026 IRS Limits)

For 2026, the contribution limits are expected to remain consistent with those set for 2024. Employees can contribute up to $16,000 annually through salary reductions, with an additional $3,500 catch-up contribution allowed for employees aged 50 and older. Employers are required to contribute annually, unlike with SEP IRAs. They can either match employee contributions dollar-for-dollar up to 3% of compensation (this can be lowered to 1% in two out of five years) or make a 2% nonelective contribution for all eligible employees.

Eligibility Requirements

To qualify, employees must have earned at least $5,000 in any two prior years. Setting up the plan involves completing either Form 5304-SIMPLE (if employees choose their financial institution) or Form 5305-SIMPLE (if the employer designates the institution). Additionally, employers cannot maintain another retirement plan during the same year the SIMPLE IRA is active. Employers are required to provide an annual notice to eligible employees between November 2 and December 31, and all contributions are immediately 100% vested.

Administrative Costs

SIMPLE IRAs come with minimal setup and maintenance costs. There’s no need to file an annual Form 5500, which reduces administrative burdens. Small business owners may also be eligible for a tax credit when they start a new retirement plan.

Tax Advantages

Employer contributions are fully tax-deductible, and employee contributions are made through salary reductions, which means they aren’t counted as taxable income for the year. However, if funds are withdrawn within the first two years, a 25% penalty applies instead of the usual 10%. This higher penalty makes SIMPLE IRAs less flexible if early access to the funds is needed.

4. Traditional IRA Plans

A Traditional IRA is a straightforward retirement savings account that anyone earning taxable compensation can set up. Unlike workplace retirement plans, this account is individually owned. For the 2026 tax year, the IRS has set the annual contribution limit at $7,500, with an additional $1,000 catch-up contribution allowed for those aged 50 and older.

Contribution Limits (2026 IRS Limits)

For 2026, the contribution cap is $7,500, and individuals aged 50 or older can contribute an extra $1,000. If you’re also contributing to a Solo 401(k) for your business, keep in mind that the Traditional IRA limit is separate from your 401(k) contributions. While both can work together as part of your savings strategy, exceeding the IRA limit triggers a 6% excise tax each year until the excess is corrected. To avoid penalties, excess contributions and their earnings must be withdrawn by the tax return deadline.

Eligibility Requirements

Anyone with taxable income can contribute to a Traditional IRA, regardless of age. Non-working spouses are also eligible to contribute, provided the working spouse earns enough to cover both contributions. Even if you’re enrolled in another retirement plan, like a SEP IRA or 401(k), you can still fund a Traditional IRA.

Administrative Costs

Setting up a Traditional IRA is relatively inexpensive. Banks, credit unions, and other financial institutions typically charge low setup fees. However, you might encounter additional costs, such as commissions or expense ratios, depending on the investments you choose. Overall, managing a Traditional IRA is less complicated compared to employer-sponsored plans.

Tax Advantages and Disadvantages

Contributions to a Traditional IRA may be tax-deductible, but this depends on your income level and whether you - or your spouse - are covered by another retirement plan. The funds grow tax-deferred, meaning you won’t pay taxes on earnings until you withdraw them. However, withdrawals are taxed as ordinary income, and you’re required to start taking Required Minimum Distributions (RMDs) by April 1 of the year after you turn 72. Early withdrawals (before age 59½) come with a 10% penalty.

To determine if your contributions are deductible, it’s essential to check your Modified Adjusted Gross Income (MAGI) against the IRS phase-out ranges. For Rockwall business owners and others, this step can clarify how much of a tax break you’ll receive. Next, we’ll compare these features with other retirement plans to help you evaluate your options.

5. Roth IRA Plans

A Roth IRA stands out from a Traditional IRA because contributions are made with after-tax dollars, meaning you won't get an immediate tax break. The reward comes later: qualified withdrawals during retirement are completely tax-free.

Contribution Limits (2026 IRS Limits)

For 2026, the contribution limit is set at $7,500, with an additional $1,100 catch-up contribution for those aged 50 or older. This brings the total to $8,600 for eligible individuals in that age group. Unlike Traditional IRAs, Roth IRAs have no age restrictions for contributions. As long as you have taxable income, you can continue funding your account.

However, eligibility is tied to your Modified Adjusted Gross Income (MAGI). For single filers and heads of households, contributions phase out between $153,000 and $168,000. For married couples filing jointly, the range is $242,000 to $252,000. If your income exceeds these limits, direct contributions may not be an option.

Eligibility Requirements

To contribute to a Roth IRA, you or your spouse must earn taxable compensation. If one spouse earns little or no income, you can still fund a Roth IRA for them, provided you file jointly and have sufficient combined earned income. Be cautious about exceeding the contribution limit, as doing so triggers a 6% excise tax each year until the excess is corrected.

Administrative Costs

Opening a Roth IRA is simple and generally inexpensive. Most banks, credit unions, and financial institutions offer these accounts with little to no setup fees. Unlike employer-sponsored plans, Roth IRAs don't require complex reporting or compliance testing. Depending on your investment choices, you might encounter costs like expense ratios or commissions, but overall, administrative fees are typically low.

Tax Advantages and Disadvantages

The biggest perk of a Roth IRA is the tax-free growth and withdrawals. Unlike Traditional IRAs, you won't owe taxes on distributions during retirement, and there are no Required Minimum Distributions (RMDs) during your lifetime. This flexibility makes Roth IRAs an excellent tool for estate planning, as you can leave funds untouched for as long as you want.

On the downside, there's no upfront tax deduction for contributions. This can feel like a disadvantage if you're currently in a high tax bracket. Additionally, high earners may face income limits that restrict or entirely prevent direct contributions, which could limit access to this retirement savings option.

6. Defined Benefit Plans

A Defined Benefit plan stands out from contribution plans by guaranteeing a specific retirement benefit. This benefit is typically calculated using a formula that factors in your salary and years of service. For Rockwall business owners with steady cash flow, this type of plan can offer much larger tax deductions compared to other retirement plans. Let’s break down its key aspects.

Contribution Limits

Defined Benefit plans don’t have fixed annual contribution limits like defined contribution plans. Instead, the IRS sets a cap on the annual retirement benefit, which is $280,000 for 2025. Contributions are determined by an actuary based on factors like your age, target retirement date, and expected investment returns. Because of this, business owners nearing retirement can contribute - and deduct - much more than the $70,000 limit seen with SEP or Profit-Sharing plans.

Eligibility Requirements

Rockwall business owners - whether they operate as sole proprietors, partnerships, or corporations - can set up a Defined Benefit plan. To qualify for tax deductions, you’ll need to adopt a formal written plan by your business’s tax-filing deadline (including extensions). The plan must comply with IRS qualification rules, including minimum coverage and nondiscrimination requirements to ensure it doesn’t disproportionately favor highly compensated employees. Generally, employees become eligible once they reach age 21 and complete 1,000 hours of service.

Administrative Costs

"A defined benefit plan provides a pre-determined benefit for participants at retirement."

While these plans allow for larger, tax-deductible contributions, they come with higher administrative expenses. You’ll need to hire an actuary to calculate funding requirements annually, which adds to the costs. Additionally, you’re required to file Form 5500-series returns each year and distribute plan documents to all eligible employees. For small businesses with 1–50 employees, there’s some relief: a tax credit can cover 100% of qualified startup costs, up to $5,000 per year for the first three years.

Tax Advantages and Disadvantages

The ability to make large, tax-deductible contributions and secure a fixed retirement income makes Defined Benefit plans appealing for business owners looking to save aggressively and reduce their tax burden. However, there are some challenges.

Mandatory contributions must be made every year, even during tough financial times. These contributions are calculated by an actuary and can vary annually, which may become a strain if your cash flow is inconsistent. Additionally, the ongoing actuarial and administrative expenses make this one of the priciest retirement plans to maintain.

7. Profit-Sharing Plans

Profit-Sharing plans give Rockwall business owners a flexible way to save for retirement. Unlike plans that require fixed contributions every year, these allow you to adjust what you contribute based on your cash flow. While they offer flexibility, they do come with some administrative responsibilities.

Contribution Limits

For 2025, you can contribute up to $70,000 annually to a participant's account. Employers can deduct contributions up to 25% of total compensation, but this is based on a maximum of $350,000 in compensation per employee. Contributions must follow a set formula, typically reflecting each employee’s share of total compensation[17, 44].

Eligibility Requirements

Profit-Sharing plans are open to businesses of all sizes in Rockwall, whether you’re a sole proprietor, partnership, or corporation. Employees are eligible once they turn 21 years old and complete 1,000 hours of service within a 12-month period. To establish the plan, you’ll need to meet your tax-filing deadline (including extensions). If you own multiple businesses, employees from those related entities may also need to be included, depending on coverage rules[17, 43].

Administrative Costs

These plans require more paperwork than simpler options like SEP IRAs. For example, you’ll need to file Form 5500 annually and pass nondiscrimination tests to ensure the plan doesn’t disproportionately benefit highly paid employees. That said, small businesses with 1–50 employees can claim a tax credit for 100% of qualified startup costs - up to $5,000 per year for the first three years[17, 43, 44].

Tax Advantages and Disadvantages

Profit-Sharing plans let you adjust or skip contributions during tough financial years without penalties. Contributions are tax-deductible for your business, and the earnings grow tax-deferred until they’re distributed. Unlike SEP IRAs, these plans allow for vesting schedules (up to six years), helping you retain employees over the long term. They can also include participant loan provisions, which SEP IRAs don’t offer. The downside? These plans require more administrative work, including annual testing and reporting.

Check out the comparison table below to see how Profit-Sharing plans measure up against other retirement options.

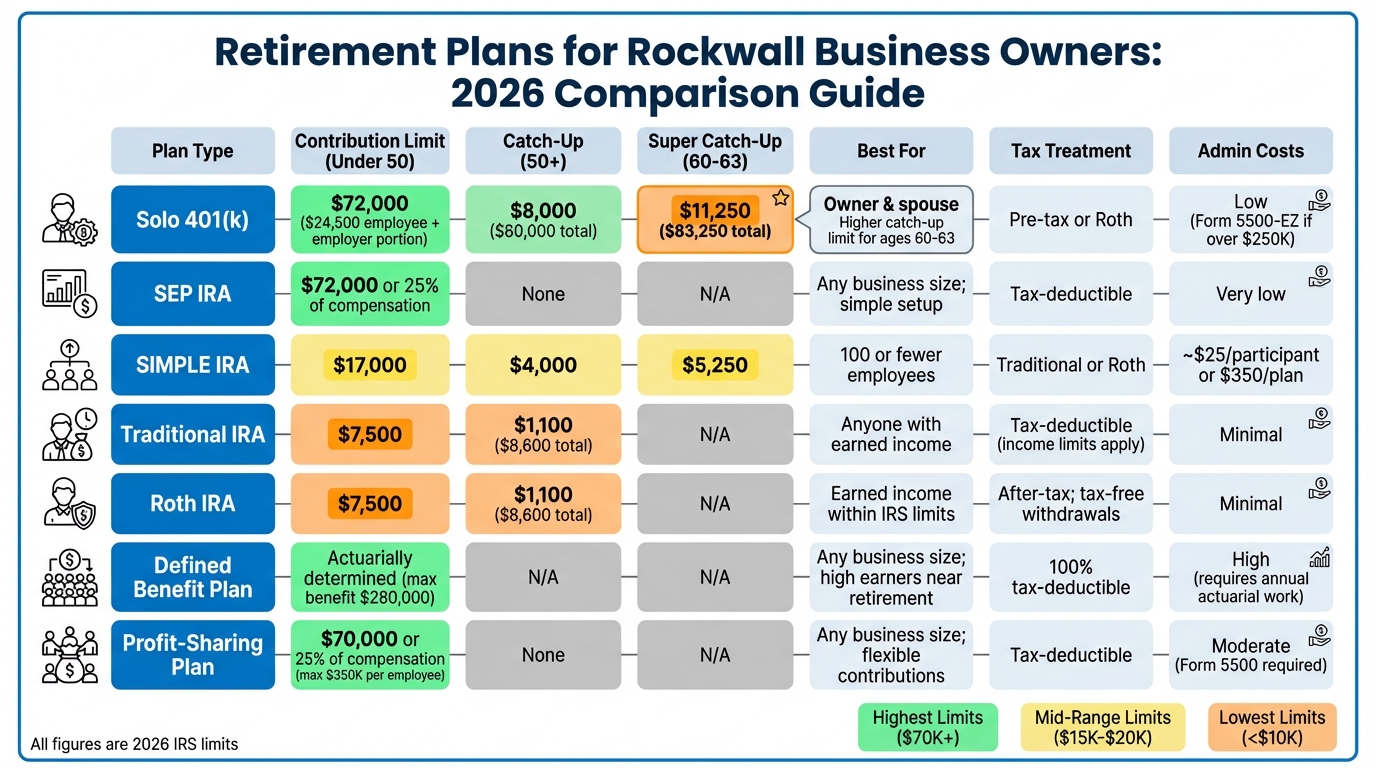

Plan Comparison Table

Designed with Rockwall business owners in mind, the table below outlines the key differences among the seven retirement savings options discussed earlier.

| Plan Type | 2026 Contribution Limit (Under 50) | Catch-Up (Age 50-59, 64+) | Super Catch-Up (Age 60-63) | Eligibility | Tax Treatment | Administrative Costs |

|---|---|---|---|---|---|---|

| Solo 401(k) | $72,000 ($24,500 employee + up to 25% employer) | $8,000 ($80,000 total) | $11,250 ($83,250 total) | Owner & spouse only | Pre-tax or Roth | Low; Form 5500-EZ required if over $250,000 |

| SEP IRA | Lesser of $72,000 or 25% of compensation | N/A | N/A | Any business size; must include eligible employees | Tax-deductible | Very low; simple setup |

| SIMPLE IRA | $17,000 | $4,000 | $5,250 | 100 or fewer employees | Traditional or Roth | ~$25 per participant or $350 per plan |

| Traditional IRA | $7,500 | $1,100 ($8,600 total) | $1,100 ($8,600 total) | Anyone with earned income | Tax-deductible (income limits apply) | Minimal |

| Roth IRA | $7,500 | $1,100 ($8,600 total) | $1,100 ($8,600 total) | Earned income within IRS limits | After-tax; tax-free withdrawals | Minimal |

| Defined Benefit | Actuarially determined (max benefit $280,000) | N/A | N/A | Any business size | 100% tax-deductible | High; requires annual actuarial work |

| Profit-Sharing | $70,000 or 25% of compensation (max $350,000 per employee) | N/A | N/A | Any business size | Tax-deductible; flexible contributions | Moderate; Form 5500 required |

Key Highlights

- Solo 401(k): Best suited for owner-only businesses, allowing contributions up to $83,250 for those aged 60-63 in 2026.

- SEP IRA: Requires equal contribution percentages for all eligible employees but does not offer catch-up contributions.

- SIMPLE IRA: Ideal for small businesses with fewer employees, though contribution limits are lower than other plans.

- Traditional and Roth IRAs: Offer simplicity and low administrative requirements, with annual contribution caps of $7,500.

- Defined Benefit Plans: Allow for the largest contributions but come with high costs due to mandatory actuarial work.

- Profit-Sharing Plans: Provide flexibility in contributions but require moderate administrative work, including filing Form 5500.

Next, explore how Rockwall's local resources can help guide you toward the best retirement savings plan for your business.

Finding Help in Rockwall

Once you've reviewed your retirement plan options, the next step is to seek local expertise to put your strategy into action. Rockwall offers a network of financial professionals who can help tailor a plan that fits your specific needs. The Rockwall Area Chamber of Commerce directory lists 17 financial professionals, giving you a solid starting point to find the right advisor.

Local advisors offer specialized knowledge that can make a big difference. Take Hooper and Rodgers, P.C., for instance. Located at 947 W. Ralph Hall Parkway, they provide retirement planning services like assessing your current assets and liabilities, determining the best time to claim Social Security, and deciding between lump-sum or monthly distributions. Another option is Gerald Hendrik at Rockwall Wealth Advisors (697 E Interstate 30), an independent fee-based fiduciary who is legally obligated to prioritize your best interests. Katie W. Brewer of Your Richest Life offers a "Fee Only" compensation model, with no minimum income or asset requirements, making her services accessible to business owners at various stages of planning. These local experts, combined with the resources on RockwallConnect.com, can help you confidently move forward.

It’s important to confirm that your advisor is a fiduciary and has experience in small business retirement planning. Many local firms can also assist in identifying tax benefits, like the $5,000 annual tax credit available during the first three years of a new retirement plan. Additionally, they can align your retirement strategy with tax planning to maximize deductions and manage Required Mandatory Distributions (RMDs) when the time comes.

RockwallConnect.com makes it easy to find the right financial advisor. Its searchable business directory provides contact details and direct links to local professionals who understand the area’s economic landscape. These advisors can offer personalized guidance tailored to your business structure, employee count, and long-term goals.

"The key to successful retirement planning is developing a plan that while based on your current financial situation, also meets your projected financial goals down the road." - Hooper and Rodgers, P.C.

Conclusion

Selecting the right retirement plan is a crucial step for Rockwall business owners. Whether you're a solo entrepreneur eyeing a Solo 401(k), managing a small team with a SIMPLE IRA, or aiming to maximize contributions through a SEP IRA or defined benefit plan, your decision should align with your business’s size, budget, and long-term goals. Each of these options provides the benefit of tax-deductible contributions and tax-deferred growth.

But it’s not just about securing your future - offering a strong retirement plan can elevate your business. It helps attract and retain top talent, giving your company a competitive edge in Rockwall’s market.

Keep in mind, retirement plans differ in terms of administrative requirements. For example, SEP IRAs are relatively easy to manage, while traditional 401(k)s come with ongoing reporting obligations. As a business owner, it’s important to weigh factors like maximum owner contributions, employee benefits, and administrative overhead before committing to a plan. Plus, small employers starting a new retirement plan might qualify for a tax credit of up to $5,000 annually for the first three years.

Navigating these decisions is easier with expert advice. Rockwall boasts a network of CPAs, financial advisors, and business attorneys who are well-versed in the local economy and can guide you through IRS regulations, tax considerations, and long-term planning. To connect with these professionals, check out RockwallConnect.com's searchable business directory.

FAQs

What should Rockwall business owners consider when selecting a retirement plan?

When selecting a retirement plan for your Rockwall business, there are a few crucial elements to weigh. Start with the tax benefits - plans often offer perks like tax deductions or tax-deferred growth. Next, review the contribution limits to ensure they fit your financial goals, and check for flexibility to adjust contributions based on your budget. Don’t overlook the administrative costs and complexity involved in managing the plan, as well as the eligibility requirements for your business and employees.

It’s also worth considering how the plan could help you attract and retain top talent. Lastly, explore whether there are any tax credits or incentives for setting up a new retirement plan. Taking these factors into account will help you choose a plan that aligns with your business needs and secures your financial future.

What are the tax benefits of different retirement plans for small business owners in Rockwall, TX?

Retirement plans for Rockwall business owners come with some great tax perks, helping you grow your savings while trimming down your taxable income. Employer contributions are generally tax-deductible, and the funds in these accounts grow tax-deferred. For employees, contributions (except for Roth accounts) aren't taxed until they're withdrawn. It's a strategic way to prepare for the future while enjoying some tax relief.

Here’s a breakdown of some popular retirement plan options:

- 401(k): This plan allows for high contribution limits and includes both employee and employer contributions. Employer contributions are tax-deductible, but the plan does require annual filings and may need nondiscrimination testing unless you opt for a Safe Harbor setup.

- SEP IRA: Employers can contribute up to 25% of an employee's compensation, and those contributions are tax-deductible. There’s no annual filing required, which makes it a straightforward option to manage.

- SIMPLE IRA: Employees contribute pre-tax dollars, and employers must either match up to 3% of compensation or contribute 2% for all eligible employees. It’s less complex to administer compared to a 401(k).

- Traditional IRA: Business owners can contribute up to the annual limit, and these contributions might be deductible on personal tax returns. The earnings grow tax-deferred, adding to its appeal.

- Roth IRA: Contributions are made with after-tax dollars, so they’re not deductible. However, qualified withdrawals are completely tax-free, which can be a big advantage later on.

Choosing the right plan for your business depends on your financial goals and cash flow. With the right choice, Rockwall entrepreneurs can reduce their tax burden while securing a comfortable retirement.

What are the costs and administrative steps for different retirement plans for small business owners?

Setting up a retirement plan for your small business comes with different levels of cost and administrative work, depending on the type of plan you go with:

401(k) Plans: These plans require a bit more effort. You'll need to adopt a written plan, set up payroll deductions, and file an annual Form 5500. Employers also have fiduciary responsibilities, like monitoring fees and choosing a record-keeper. Costs can include setup fees ranging from a few hundred to several thousand dollars, plus ongoing administrative fees that typically fall between 0.5% and 1.5% of plan assets.

SIMPLE IRA: Designed for businesses with 100 or fewer employees, this option is easier to manage. Employers either match employee contributions up to 3% of compensation or make a flat 2% contribution. Administrative requirements are minimal, and costs are generally limited to account setup and custodial fees. There’s no need to file annual forms, which keeps things straightforward.

SEP-IRA: Perfect for self-employed individuals or businesses of any size, this plan allows employers to make discretionary contributions - up to 25% of compensation or $66,000 for 2024. The paperwork is light, requiring only a simple election form, and costs are usually limited to standard custodian fees for IRAs.

Traditional or Roth IRAs: These are individual accounts rather than employer-sponsored plans. For business owners, the process is as simple as opening an account with a financial institution. Costs are generally limited to small account setup or maintenance fees, making these accounts an easy and affordable choice.

Each type of plan has its own perks and requirements, so it’s important to pick the one that aligns best with your business goals and resources.

Related Rockwall Businesses

-

Lead Fuel CRM

Your Entire Business in One App. Phone, email, text, invoicing, contracts, automation, AI, websites, funnels, reviews, s

-

PxlPerfect Designs

At PxlPerfect Designs, we believe in more than just websites and SEO - we believe in helping businesses grow, supporting

-

Dr. Charles M. Russo, PhD

I teach business leaders and entrepreneurs to make better decisions through sharpening critical thinking skills . Provid

-

Home Flex Media

We are a real estate media team that specializes in luxury homes. We create listing photos and marketing videos for you

-

PLF Art Services

PLF Art Services. Our mission is simple: to help your business get SEEN, RECOGNIZED and CHOSEN to INCREASE YOUR REVENUE.

-

Arctic Spas Rockwall

Hot Tubs, swim Spas & Coldtubs Engineered For The World's Harshest Climates